News

Stay up to date on the latest crypto trends with our expert, in-depth coverage.

1Bitget UEX Daily|Micron Earnings Significantly Beat Expectations Boosting AI Sentiment; Oil Prices Fall as Supply Concerns Ease; Trump Delays Housing Bill Signing2Micron Technology (MU) FY2026 Q3 Earnings: Revenue Surges 346% YoY, Gross Margin Hits Record 84.9%, Q4 Guidance Crushes Estimates3The "Storage Supercycle" in Kioxia's Financial Report: Apple Orders Surge, Raw Material Inventory Soars, and the Entire Industry Chain Is Rushing to Position Ahead

US Bitcoin ETFs Attract $2 Billion in July, Surpass 900,000 BTC in Holdings

BeInCrypto·2024/07/21 10:31

Bitcoin Price Analysis: Here’s the Next Target for BTC Before Bulls Can Hope for $70K

Cryptopotato·2024/07/21 07:47

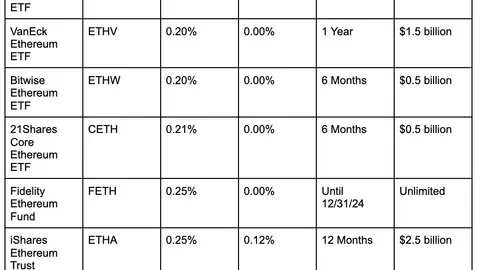

Ethereum ETFs are coming — Here’s what you need to know

Are you ready for the July 23 launch of nine spot Ethereum ETFs? Here's what you need to know to start trading.

Cointelegraph·2024/07/20 19:52

Ethereum’s spot ETFs will trigger a dip, not a rally

Share link:In this post: Ethereum’s supply has been increasing by 60,000 ETH per month since April, which could lead to a market dip instead of a rally when spot ETFs are introduced. Historical patterns from 2016 and monetary policy trends suggest that ETH/BTC might see a huge drop before potentially rising next year. Benjamin Cowen warns that if the current supply trend continues, Ethereum’s supply will revert to pre-Merge levels by December 2024.Disclaimer. The information provided is not trading advice.

Cryptopolitan·2024/07/20 18:13

If Joe Biden bails on the presidential race, what’s next?

Cryptopolitan·2024/07/20 18:13

Is It Too Late To Buy TURBO? Turbo Price Skyrockets 45% As Traders Rush To Buy This AI Crypto Before It’s Too Late

Insidebitcoin·2024/07/20 17:56

Bitcoin Shines as ‘Blue Screen of Death’ Cripples Global Systems: Senator Lummis Reacts

Coinedition·2024/07/20 14:55

The Trump Effect: Bitcoin, Solana, XRP Soar on Renewed Investor Optimism

Coinedition·2024/07/20 14:55

Bitcoin Whales Signal Bullish Trend: $5.6 Million Options Bet Fuels Price Rally

Coinedition·2024/07/20 14:55

Can Ethereum ETFs Propel ETH Price to $4,000?

Newscrypto·2024/07/20 14:52

Flash

08:35

On June 25, the onshore RMB closed at 6.7995 against the US dollar, up 57 basis points.On June 25th at 16:30 (UTC+8), the onshore RMB closed at 6.7995 against the US dollar, up 57 points from the previous trading day.

08:34

US Stock Market Movement: NEBIUS surges over 4% pre-market after launching its self-developed AI agent, Nebius EchoGolden Ten Data June 25|Artificial intelligence cloud service provider NEBIUS (NBIS.US) rose more than 4% pre-market, quoted at $270.08. In the news, NEBIUS launched version 3.6 of Nebius AI Cloud, codenamed Aether, bringing major feature upgrades to AI business teams in production environments, and simultaneously opened a preview channel for developers’ co-creation program and dedicated certification system. The company introduced its self-developed AI agent, Nebius Echo, which supports controlling cloud infrastructure with natural language and is natively integrated into the web console. In the future, it will gradually cover intelligent troubleshooting and automated code deployment functions. (Golden Ten Data)

08:28

Goldman Sachs: Divergence Emerges in AI Trading as Market Scrutinizes Capital ReturnsBlockBeats News, June 25, Goldman Sachs strategists believe that Wall Street's AI trading is entering a more complex phase: the market still believes in the AI investment cycle, but no longer puts all AI companies into the same valuation framework. Over the past year, the most favored investments among investors have been the direct beneficiaries in the AI infrastructure chain. Nvidia, TSMC, and some semiconductor equipment and server suppliers have benefited from continued capital expenditure increases by major cloud computing companies. As long as Amazon, Alphabet, Meta, and Microsoft continue to purchase chips, servers, and data center capacity, the revenue outlook for hardware companies will remain supported. However, the hyperscalers themselves, who shoulder these expenses, have not seen equally strong stock performance. The market is rewarding "the side that collects money," but remains cautious about "the side that spends money." Investors are increasingly concerned about whether these hundreds of billions of dollars in AI investments can ultimately be converted into profits, free cash flow, and shareholder returns. This is what Goldman Sachs refers to as AI trading being like a "stretched rubber band." On one end, orders and profit expectations for hardware suppliers are continuously being elevated; on the other, large tech platforms are under increasing capital expenditure pressure. As long as AI demand keeps growing, this dynamic can continue. But if the market starts to doubt the investment return rate, or if cloud giants signal a peak in AI spending growth, related stocks may be repriced. Goldman Sachs is not bearish on AI, but believes that AI trading has moved from thematic investing to a stage of verifying returns. The market no longer just asks "who is involved in AI," but is now concerned with "who can actually make money from AI." For Nvidia, TSMC, and the AI device chain, the biggest risk is not vanishing demand, but that demand growth may no longer continually exceed expectations. For Amazon, Alphabet, Meta, and Microsoft, the short-term pressure comes from excessive capital expenditure; however, if AI costs decrease, or AI products bring in clear revenues, they might instead become the next beneficiaries. The bigger variable is the AI cost curve. If China, Japan, or other regions can develop and run high-performance models at lower costs, the current high capital expenditure path of major U.S. tech companies might be challenged. The market has previously assumed that leading AI always requires more chips and larger data centers, but improvements in model efficiency and the development of alternative chips could undermine this logic. Therefore, the main AI narrative hasn’t ended, but the buying logic is becoming more refined. The next phase is not merely about whether there is AI demand, but about who can turn AI investment into real cash flow.

News